In navigating the complex landscape of economic forecasting and market analysis, the insights provided by Ironsides Group offer invaluable guidance for stakeholders seeking clarity amidst uncertainty.

As the U.S. economy charts its course through the intricate interplay of growth, inflation, and monetary policy, Ironsides Group presents a comprehensive outlook for Q1 2024 and beyond.

Within this context, this executive summary encapsulates key economic indicators, forecasts, and projections, providing a nuanced understanding of current trends and future trajectories.

By delving into the intricacies of GDP growth, inflationary pressures, and their implications on real estate and capital markets, Ironsides Group equips decision-makers with actionable intelligence to navigate the evolving economic landscape with confidence and foresight.

Executive Summary: Ironsides Group Outlook

1. In Q1 2024, U.S. GDP saw a modest increase of 1.6% on an annualized basis, falling short of market projections set at 2.4%.

2. Accompanying this subdued growth was persistent inflation, with the Core Personal Expenditures Price Index registering at 3.7% annualized in Q1. While this surpassed the Federal Reserve’s 2% target, it aligned closely with Ironsides Group’s forecast of 3.6%. The steadfast nature of inflationary pressures will likely keep the Fed cautious, delaying any potential rate cuts until July.

3. Ironsides Group anticipates a slowdown in the U.S. economy throughout the year, yet foresees a controlled deceleration rather than a recession. Nonetheless, stringent monetary policies will pose significant challenges.

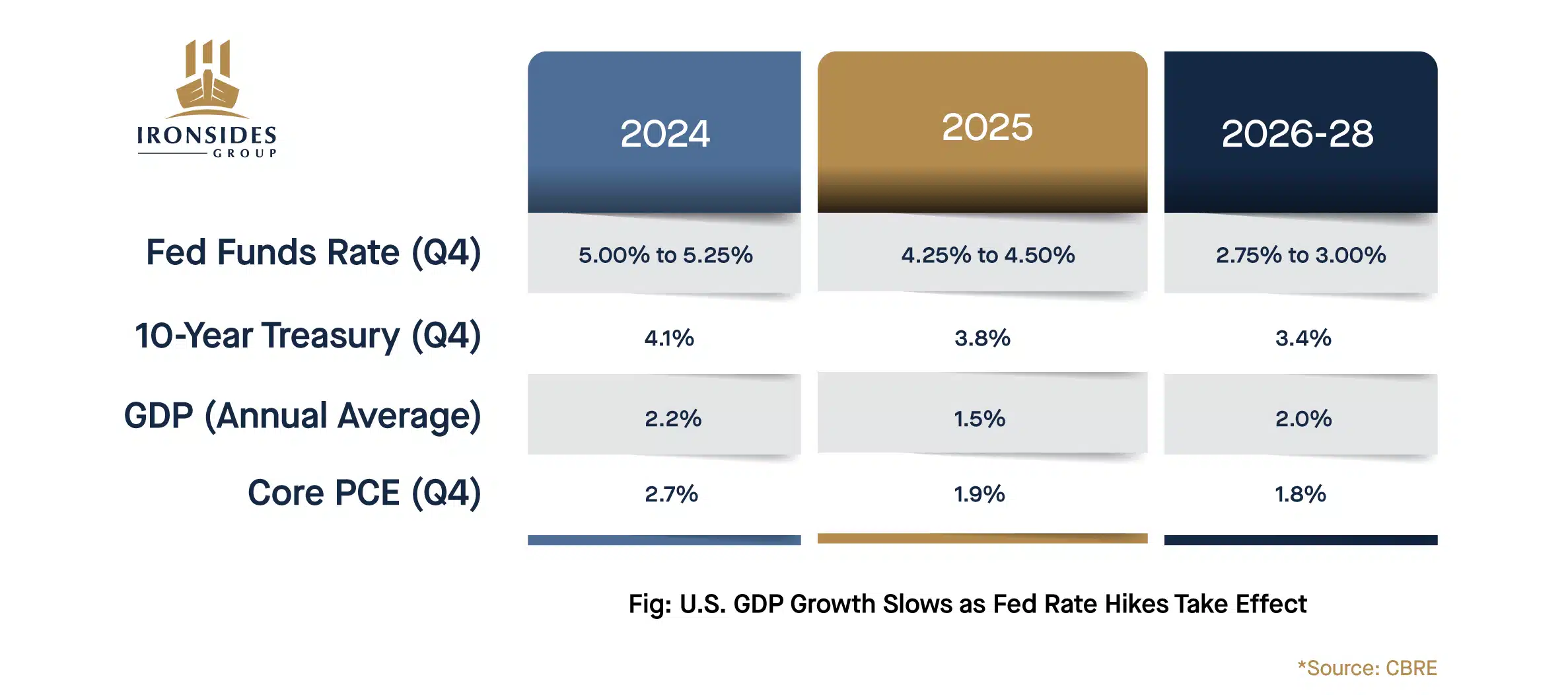

4. Projections suggest a gradual alleviation of inflation in Q2, prompting a steady decline in the 10-year Treasury yield to reach 4.1% by year-end. Despite high interest rates dampening real estate investment activity in the first half, a modest recovery may ensue in the latter part of the year.

The subdued Q1 GDP growth establishes the trajectory for 2024.

Reduced inventories and sluggish trade activities contributed to the lower-than-expected growth rate of 1.6%, diverging from Wall Street’s anticipation of 2.4%. While consumer spending, residential investment, and government expenditures all slowed, they remained contributors to GDP growth.

Notably, consumer spending shifted towards services over goods. Additionally, the Core Personal Consumption Expenditures Price Index saw a more significant increase than anticipated, reaching 3.7% annualized in Q1.

Ironsides Group’s Outlook

Despite GDP growth falling short of expectations, core PCE inflation maintained levels above the Fed’s target, while jobless claims decreased in Q1. These dynamics raise concerns of potential stagflation, mirrored by the continued ascent of the 10-year Treasury yield.

Ironsides Group’s outlook continues to envision a soft landing for the economy, characterized by subdued growth and moderated inflation in 2024. Anticipated improvements in inflation metrics next month may prompt the Fed to enact a 25 basis point reduction in the federal funds rate come July.

This move is expected to mitigate volatility in bond markets, facilitating a gradual decline in the 10-year Treasury yield, projected to culminate at 4.1% by the year’s end.

Ironsides Group anticipates modest growth in industrial and office leasing activity for the year. However, high interest rates will persist as a barrier to capital markets activity.

Investment trends are anticipated to mirror those of the previous year, with a slight uptick expected in the latter half of 2024, paving the way for a more robust recovery in 2025.